ESTIMATING YOUR FEDERAL ESTATE TAX

You can estimate your federal estate tax liability by developing your own worksheet. First, calculate the present value of your gross estate by adding up these assets:

· Stocks, bonds, real estate, and cash.

· Household furnishings, motor vehicles, jewelry, and collectibles.

· Proceeds from life insurance policies and annuities.

· Retirement benefits including Individual Retirement Arrangements (IRAs) and employer-sponsored pension and savings plans.

· Gifts you've made with “strings attached.” For instance, if you give your home to your daughter, but retain the right to occupy it for life, the Internal Revenue Service (IRS) would say the home is really yours.

· Property in a revocable trust.

· Assets over which you hold general power of appointment. For example, your father and mother put stock in a trust over which they give you general power of appointment. Since the power of appointment would permit you to distribute the shares to anyone, including yourself, the IRS considers the stock yours, even if you never touch it.

· Your share of jointly-held property. If you own an asset with your spouse that he or she will automatically inherit upon your death, half of its value is included in your taxable estate. If your co-owner is someone other than your spouse, and together you received the property as a joint gift or inheritance, half of its value also ends up in your estate. If you purchased the property together, the portion you paid for is part of your estate.

If you live or have lived in a community property state (i.e., Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), all income earned and assets acquired by a married couple living in one of those states, except for individual gifts and inheritances, are considered community property and half of it is included in each spouse's estate.

The next step in estimating your federal estate tax is to calculate your outstanding debts:

· Mortgage balances and other loans.

· Liens on your real estate.

· Income and property taxes and credit card balances.

· Estimate funeral expenses and the cost of settling your estate.

· Court costs; attorneys, executors, accountants, brokers, and appraisers fees (usually 5 to 10 percent of your adjusted gross estate).

To calculate your adjusted gross estate, subtract all your debts and final expenses from your gross estate.

Now, you can leave your entire estate to your spouse, tax free, because of the marital deduction. If you choose to do so, your spouse should then fill out a photocopy of the worksheet that you have developed to see if estate taxes will be due when he or she dies.

To calculate your taxable estate, add any taxable gifts made after 1976 to your adjusted gross estate and subtract your marital deduction and charitable bequests. You can make tax-free gifts up to $10,000 a year each to as many people as you'd like. Married couples may jointly give as much as $20,000. Prior to 1982, when those amounts took effect, the limits were $3,000 for individuals and $6,000 for married couples. To determine the amount of taxable gifts you've made, check the gift tax returns that you should have filed after making the gifts.

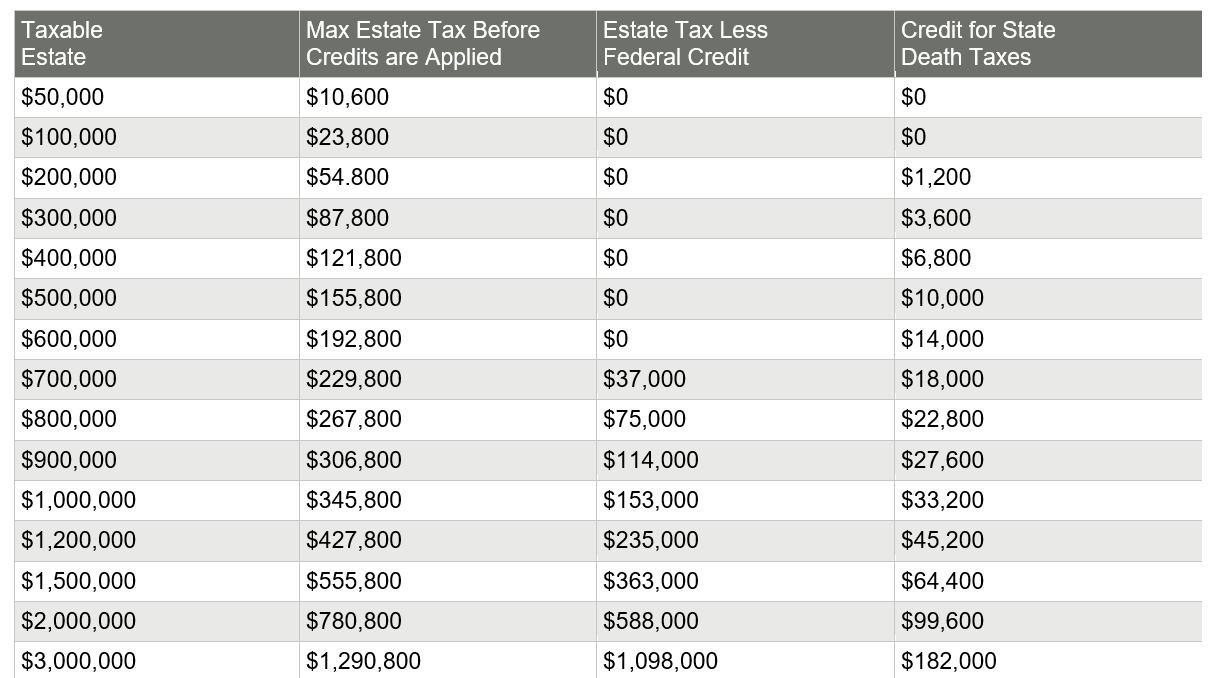

You can now use the table below to estimate your tax bill. For those estimated above $600,000 brackets range from 37 percent to 55 percent. If your taxable estate totals $800,000 (Column A of the table), the federal estate tax, before any credits are applied, would be $267,800 (Column B). You're entitled to a $192,800 federal credit against gift and estate taxes. If you've paid any federal gift tax after 1976, subtract that as well. See Column C for your federal estate tax minus the federal credit and plug that into the calculation. Finally, you may deduct a $22,800 credit for state death taxes (Column D). The federal government's share of your estate in this case is $52,200.

While income taxes may be a certainty, estate taxes need not be. In fact, you can escape the federal estate tax entirely by making sure that the value of your taxable estate is below $600,000. Federal taxes on estates under that amount are entirely offset by a $192,800 credit which is available to everyone. That does not mean, however, that you can avoid the tax by just giving away everything but $600,000 when you die. The federal estate and gift taxes are unified, meaning that the value of taxable gifts as of the time you made them will be added to the property you hold at death in calculating your estate tax liability.

Fortunately, the tax law allows you many options. You may give as much as $10,000 a year, each, to as many people as you wish without incurring the gift tax. Married couples can jointly give up to $20,000. You may also make tax-free gifts of any amount to charities and unlimited payments to health care and educational institutions to cover a relative or friend's medical or tuition bills.

An even larger opportunity is the marital deduction which allows you to give during your lifetime, or bequeath at your death, as much as you want to your spouse, tax free, as long as he or she is a U.S. citizen. The write-off has its limitations though. If your spouse ends up with more than $600,000, you may only postpone the estate tax until his or her death.

One way to solve the problem is through the judicious use of trusts. For example, a bypass trust--sometimes called a family or credit shelter trust--allows both partners in a marriage to take advantage of their separate $600,000 estate tax exemption to pass as much as $1.2 million to their heirs tax free. In this arrangement, you bequeath assets worth up to $600,000 tax free to the trust. The remainder goes directly to your spouse and because of the marital deduction that bequest also escapes taxes.

For the rest of your spouse's life, he or she can collect the trust's income and usually up to $5,000 or 5 percent a year of the principal, whichever is greater. After your spouse's death, your children or other heirs become the trust's beneficiaries. But, because the trust was not under your spouse's control, the assets do not count toward his or her taxable estate. And, as long as your spouse's own assets are less than $600,000, your estate passes from you to your spouse to your children free of federal estate taxes.

The above suggestions allow an individual only to estimate federal estate taxes. It is no substitute for a complete estate and financial plan. Professional advice is required to ensure your heirs and beneficiaries will receive as much as possible.